Search our website enhanced by Google.

Thursday, 9 January 2020

By Chris Gooderham

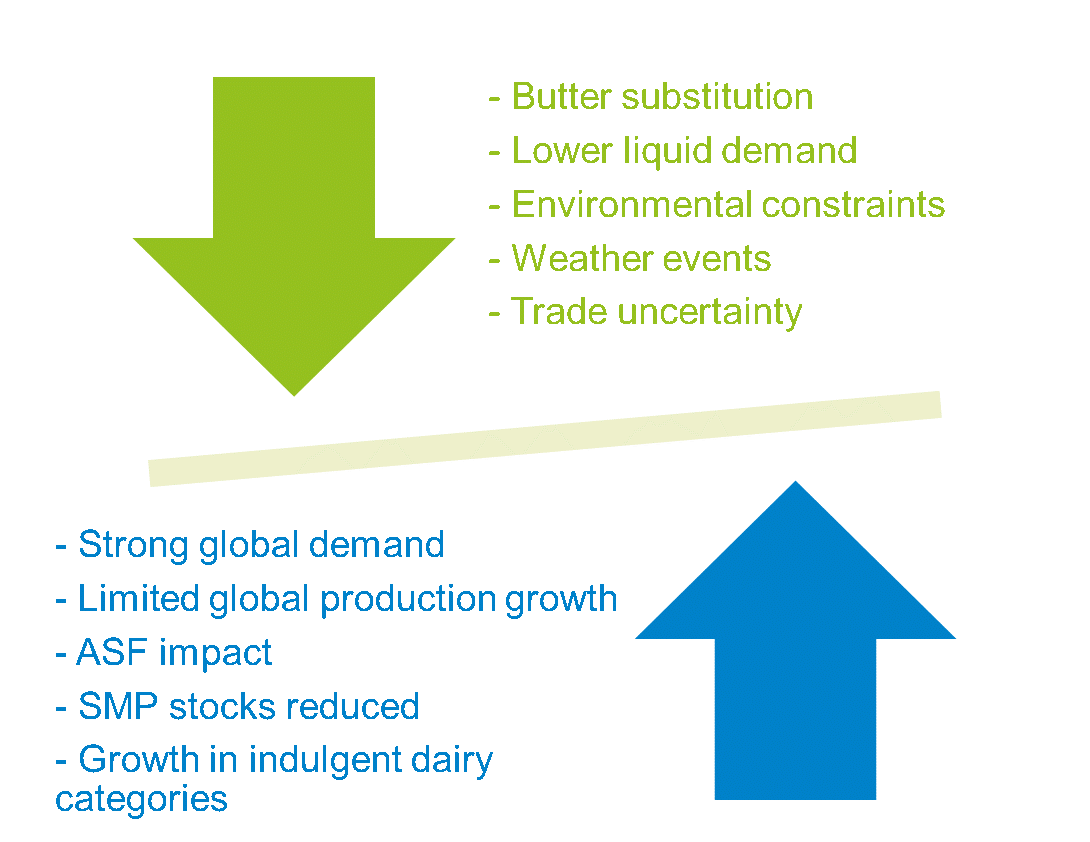

Despite the uncertainty in 2019, the market value of milk in the UK was the most stable it’s been for a decade. But as we enter the next decade, how long will that stability last? We take a look at the key dynamics that are playing out in the dairy markets at the moment.

2020 will be the start of a new era for the dairy industry, with many challenges and opportunities already starting to develop. Extreme weather events will likely become more frequent and continue to impact production, while environmental concerns will increasingly drive consumer decisions around food choices.

Changes will need to be made to food supply chains to meet the Government’s pledge to be net zero by 2050, and we can expect to see both political and consumer pressure on food producers to help the country meet this challenge.

We will also see the implementation of measures by some milk processors to ban the euthanising of healthy bull calves on farm. This has implications for breeding and inseminations decisions, production costs and the beef supply chain. It could also impact milk production levels further down the line.

As we exit from the EU, the UK supply chain will need to reassess its view of demand from consumers both domestically and internationally. This may require an adjustment in milk utilisation to ensure we are producing the right products for the right consumers. As the proportion of milk used for manufactured products increases, compared with the liquid market, the importance of milk solids will become ever more evident.

This reassessment also gives the industry an opportunity to decide what information it needs to compete, while giving the right level of transparency for everyone in the supply chain to support decision making in the uncertain years ahead.

Our Dairy Markets Weekly publication will continue to keep you informed about the key factors influencing the market. Ensure you are on the subscription list by managing your preferences here.

Sign up to receive the latest information from AHDB.

While AHDB seeks to ensure that the information contained on this webpage is accurate at the time of publication, no warranty is given in respect of the information and data provided. You are responsible for how you use the information. To the maximum extent permitted by law, AHDB accepts no liability for loss, damage or injury howsoever caused or suffered (including that caused by negligence) directly or indirectly in relation to the information or data provided in this publication.

All intellectual property rights in the information and data on this webpage belong to or are licensed by AHDB. You are authorised to use such information for your internal business purposes only and you must not provide this information to any other third parties, including further publication of the information, or for commercial gain in any way whatsoever without the prior written permission of AHDB for each third party disclosure, publication or commercial arrangement. For more information, please see our Terms of Use and Privacy Notice or contact the Director of Corporate Affairs at info@ahdb.org.uk © Agriculture and Horticulture Development Board. All rights reserved.

Topics:

Sectors:

Tags: